This post is sponsored by Thrive Market, an online platform that can save you up to 50% on your favorite organic groceries.

Anybody else out there feel a bit squeamish about your bank account after your landlord deposits the rent check?

No question, paying your monthly rent (or—if you’re one of the lucky ones—your monthly mortgage) means your account balance takes a huge hit. And after a particularly bad month of binge spending and flash sales, it can feel less like "Woah, money's going to be tight this week" and more "Please, please don't charge me another overdraft fee."

Too often, when money's tight, we choose the route of denial. If you’ve ever floated yourself with a credit card until that glorious check on the 15th (you know, the one where there’s no rent due and it suddenly feels like you came into a small inheritance), you know what I mean. But taking charge of your budget woes doesn’t have to be hard or emotionally heavy.

The trick? Small shifts that you barely notice but that ultimately pay off, literally. Here are a few you can try starting today:

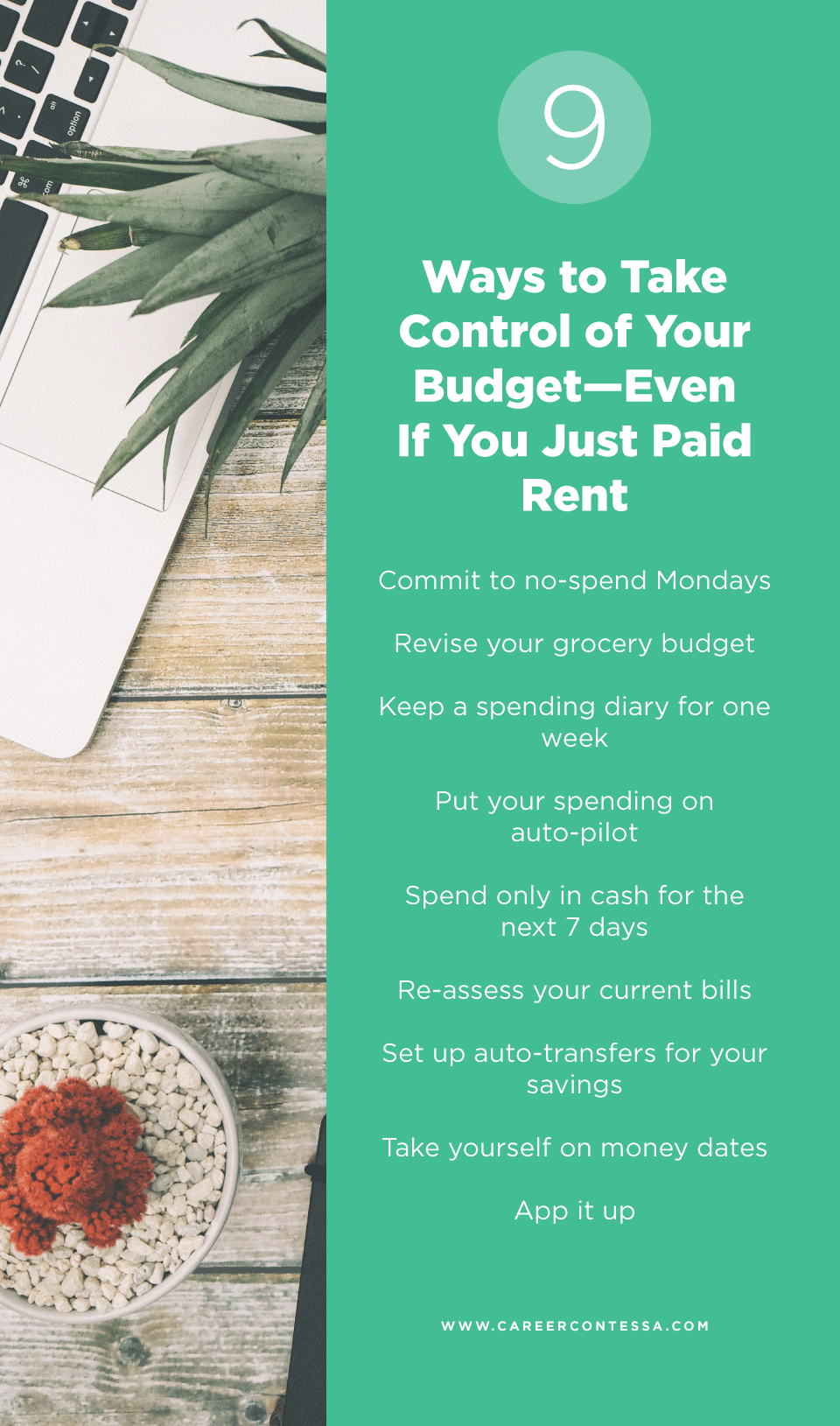

1. Commit to No-Spend Mondays

Having a day of the week where you don’t open your wallet can dramatically change the state of your bank balance over time. Some people swear by No Spend Months (usually as a New Year’s Resolution) to pay off large chunks of debt, but dedicating even a day a week adds up. Mondays are great for this because you’re coming down from the thrills of the weekend and are less likely to have social plans at night. But, of course, feel free to go no-spend on a Tuesday or a Thursday instead. Whatever is easier for you is going to work best in terms of sticking to it.

2. Revise Your Grocery Budget

Erratic trips to the grocery store and that wasted produce add up to a huge chunk of change. If you’re not paying attention to pricing or shopping out of convenience rather than with intention, you’re probably missing opportunities to save hundreds of dollars. A study by the American Dairy Association Mideast reports that American families waste around 250 pounds of food every year.

So, yeah, being hyper-vigilant about tracking your food spending can change your entire budget. Cue the How to Set a Food Budget worksheet, which we’ve designed with Thrive Market to help you realign your budget, assess where you’re spending too much, and better plan your purchases. Download it here:

3. Keep a Money Diary For One Week

Just for seven days. You can even do this in the Notes app on your phone. The idea here is to write down everything you spend (yes, even that $2.00 parking meter), so you can see exactly how it all adds up. You'll start to see patterns, like how much money you lose when you buy an item at your local store but could have bought it for half that price on Thrive Market. Keeping a diary also has positive psychological effects: not only will taking note of what you’re spending make you rethink certain decisions, but it also gives you a better idea of what your weeks look like, so you can plan accordingly.

4. Put Your Spending On Auto-Pilot

What are some things you purchase every month? Toilet paper. Face wash. Olive oil...

If you find yourself just grabbing all these things at once from a big box store, you’re probably missing some great opportunities to save some major bucks. By planning in advance and ordering online, you can get the most bang for your buck.

This goes for groceries, too. Most of the products on Thrive Market’s platform cost 25-50 percent less than they do in brick and mortar stores. The other added bonus of buying online is that you’ll be less tempted to add impulse buys to your cart like you would be in a store (hello, snack aisle—did you know grocery stores are laid out to tempt you?).

Look, if you really need that kettle corn and those chocolate peanut butter cups, we see you. But again, if you buy online via Thrive Market, you’ll get those splurges for much, much less.

5. Spend Only in Cash for the Next 7 Days

Debit cards are highly convenient, but they also make it easier for you to ignore what’s going on with your spending. Try this: calculate a budget for the week that you believe is fair/doable or just withdraw a couple hundred bucks from your checking account. Over the next few days, pay only in cash. You’ll be shocked at how fast it goes but also much more conscious of where and when you’re doling out your money.

6. Re-assess Your Current Bills

Often, just calling your internet provider or credit card company is enough to get a reduced monthly bill or interest rate. We just assume it's not going to help to ask. So go ahead, set aside an hour, and make a few calls.

Also, check to see what recurring fees you're automatically paying. There are probably some must-haves there, but there may be some superfluous ones as well.

What subscriptions are valuable and/or make your life better? Whether it’s your beloved Netflix subscription (AKA your favorite way to unwind) or your Thrive Market membership (which truly helps keep your grocery shopping organized and on budget), those are the recurring bills you’ll want to keep paying. But next, think about the ones that aren’t important. Are there any apps or services that you haven't used in ages? Do you really need commercial-free Spotify when you only use it a couple times a week? Anything you can cut, do.

7. Set Up Auto-Transfers for Your Savings

This advice comes from one of our favorite women, Ashley Feinstein of The Fiscal Femme. Sometimes, the savviest choices are also the simplest. Feinstein argues that the best thing you can do for your financial health is “pay yourself first.” This month, determine what your savings goals are, then set auto-transfers from your checking account (either weekly or monthly) to pull that money out before you have time to spend it.

8. Take Yourself on Money Dates

This is something Thrive Market staffer, Lily Comba, told us she does every month, and we’re obsessed. Says Comba, “I'll get a nice glass of wine, some snacks (from Thrive Market, duh) and do a check-in with my finances. How am I spending? How am I saving? You can also put alerts in your phone for every week at a certain time to just check your bank account."

That may seem strange, but it shifts how you're thinking about your finances. Says Comba, "Your relationship with money is like any other relationship—it takes time and a lot of love, and making it a part of your day, week, month will transform how you feel. And when you feel good about your money, you're more comfortable talking about it (hello, ask for that raise!)”

9. App It Up

Self-control is a great thing to strive for, but there are also ways to help yourself if you tend to give in to temptation. Try downloading a personal finance app like You Need a Budget.

Whether you'd rather tuck away some extra pennies by rounding up every purchase to the next whole dollar, or you want small sums to be withdrawn on the down-low—there's an app that can help you do it. Actually, we have 10 favorites.

One Last Note: Stop The Negative Talk

Try a few of these tips and see what happens. But above all else, stop saying you're "bad with money" or calling yourself "broke." The self-bashing doesn't help. By turning your attention to how you're going to affect change and paying attention to small ways you can take more of an active role in your budget and savings, you'll immediately start to feel better. Because knowledge is power, right?

This post is sponsored by Thrive Market, an online platform that can save you up to 50% on your favorite organic groceries.